Abercrombie & Fitch Co. (NYSE: $ANF), the young adult apparel retailer known for brands like Abercrombie Kids, Abercrombie & Fitch, and Hollister, reported impressive fourth-quarter fiscal 2025 earnings on March 4, 2026, before the market opened. The results showed continued brand strength, robust holiday demand, and operational execution, building on a multi-year turnaround under CEO Fran Horowitz.

With net sales reaching record levels and EPS beating expectations, the company reaffirmed its position as a standout performer in the apparel sector despite broader retail challenges like cautious consumer spending and potential tariff impacts.

Key Financial Highlights for Q4 Fiscal 2025

Abercrombie posted record quarterly net sales of $1.585 billion, up 9% year-over-year on a reported basis and 10% in constant currency. Comparable sales surged 14%, driven by strong traffic, lower promotions, and positive customer response to holiday assortments. Hollister led the charge with 16% sales growth and 24% comps, while Abercrombie brand sales rose 2% with 5% comps.

Gross margin came in at 61.5%, down from 62.9% a year earlier, primarily due to higher freight costs and increased air shipments to meet demand. Operating margin expanded to 16.2%, up 90 basis points year-over-year, reflecting disciplined expense control. Diluted EPS reached $3.57, up 20% from the prior year and ahead of consensus estimates around $3.50–$3.56.

The quarter capped a strong fiscal 2025 overall, with full-year performance showing consistent momentum from product innovation, digital enhancements, and store optimizations.

Holiday Performance and Brand Momentum

Management highlighted a “strong customer response over the holidays,” with record quarter-to-date sales through December aligning with expectations. The team stayed “on offense” across product, marketing voice, and in-store/digital experiences, leading to high traffic and conversion without heavy discounting.

Hollister’s outsized growth reflected successful appeals to younger demographics through fresh styles and targeted campaigns. Abercrombie brand progress, though more modest, benefited from premium positioning and loyalty gains. Inventory management remained disciplined, supporting healthy margins despite supply chain headwinds.

These results underscore Abercrombie’s turnaround story, shifting from past struggles to consistent growth through curated assortments and omnichannel strength.

Guidance and Outlook for Fiscal 2026

Looking ahead, Abercrombie provided conservative yet positive guidance for fiscal 2026 amid tariff uncertainties and macro caution. The company expects net sales growth of 3–5%, operating margin in the 14–15% range (down slightly from prior peaks due to carryover costs and freight), and EPS of $10.40–$11.40.

For Q1 2026, sales growth is projected at 4–6%, with operating margin 8–9% and EPS $1.25–$1.45. The outlook incorporates about $90 million in estimated tariff expenses for the year (roughly 170 basis points of sales impact, net of mitigation), assuming current trade policies.

The company also announced a new $1.3 billion share repurchase authorization, targeting ~$100 million per quarter in 2026 (subject to conditions), signaling confidence in cash flow and balance sheet strength. Capital expenditures are planned around prior levels to support store openings, remodels, and digital investments.

Market Reaction and Broader Implications

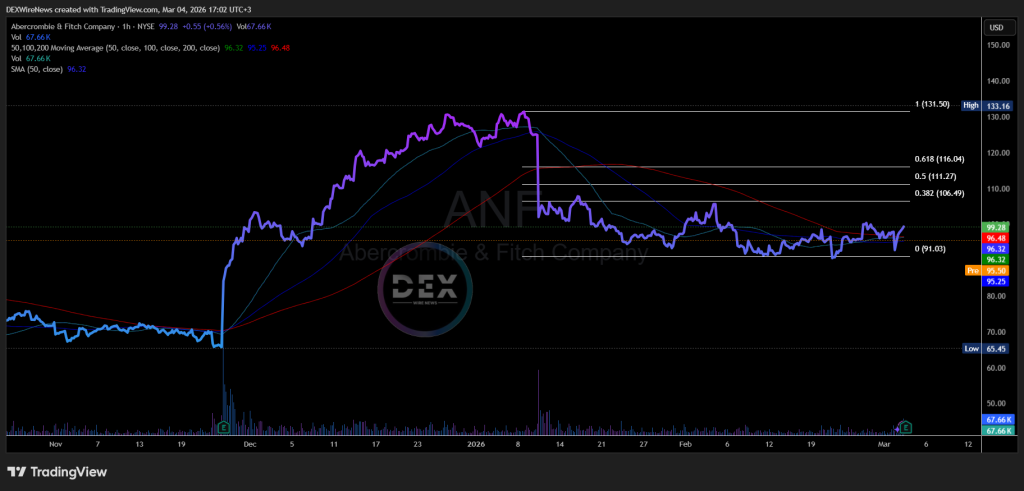

Shares of ANF reacted positively to the results and guidance, with pre-market and early trading showing gains as investors rewarded the record performance and buyback news. The stock has been a strong performer in recent years, though it traded below some analyst targets heading into the report (average around $123 vs. recent levels near $97–$100).

In a mixed retail environment, where discretionary spending faces headwinds from inflation and economic uncertainty, Abercrombie’s results offer a positive signal. Strong comps and margin expansion demonstrate pricing power and brand loyalty, potentially influencing peers in apparel and youth fashion.

Key coverage angles include same-store sales trends (robust at 14%), inventory discipline (supporting margins), and the outlook for consumer durability amid potential tariffs. The company’s ability to grow on top of prior records while navigating costs positions it well for sustained momentum.

Abercrombie & Fitch’s Q4 report reinforces its status as a retail bright spot, with execution driving record results and a clear path forward despite external pressures.

Click Here for Updates on ANF – It’s 100% FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment. Please read our Full Disclaimer: https://dexwirenews.com/disclaimer/