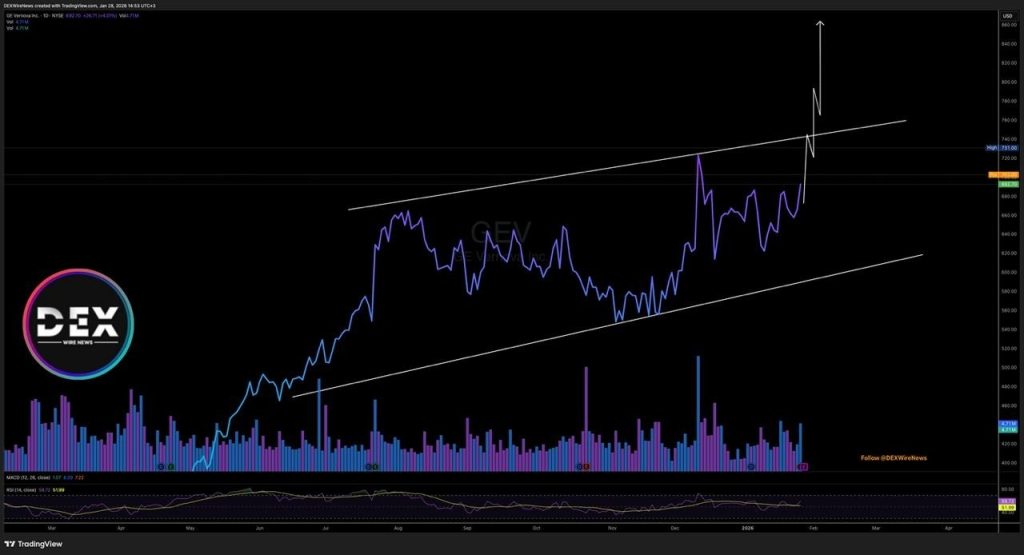

GE Vernova (NYSE: $GEV) reported strong fourth-quarter 2025 financial results this week, showing revenue, orders and cash flow growth as the energy equipment maker benefits from steady demand for power systems, grid electrification and related infrastructure. The performance comes after a strong run in the stock, GEV shares have climbed roughly 100%+ over the past year as investors bet on rising energy equipment demand, including projects tied to data centers, utilities, and broader electrification trends.

The company’s earnings beat Wall Street’s expectations on several key fronts. In Q4, GEV reported about $11.0 billion of revenue, a modest year-over-year increase, and generated strong net income of roughly $3.7 billion, helped by one-time tax benefits. Orders jumped sharply, with $22.2 billion in new orders, up more than 60% organically, reinforcing the view that demand remains solid across markets where utilities and industrial customers are investing in power equipment. Free cash flow also improved significantly as operating cash trends strengthened.

Strong Backlog and Rising Guidance Suggest Continued Momentum

One of the most important takeaways from the results is the huge backlog growth. GEV’s total orders and backlog, equipment and services waiting to be delivered, climbed to about $150 billion, up sharply from earlier periods.

A large backlog helps signal future revenue visibility because it means the company already has a significant pipeline of contracted work that should convert to revenue as projects are executed.

Management also provided an upward revision to 2026 guidance, forecasting higher sales and free cash flow than previously expected. GE Vernova expects roughly $44–$45 billion in revenue in 2026, with adjusted EBITDA margins of 11–13% and continued strong cash generation. The multi-year outlook out to 2028 was also raised, reflecting confidence in long-term demand for its power, electrification, and grid equipment solutions.

Why Energy & Infrastructure Demand Matters

The strong earnings and guidance reflect broader trends in energy infrastructure spending. Utilities and large industrial projects, including data centers, manufacturing facilities, and electrification projects, have continued to boost demand for gas power turbines, grid electrification equipment, and related services.

Growth in artificial intelligence infrastructure in particular has fueled electricity usage and capital spending on reliable, scalable power systems. This has helped companies like GEV capture solid growth in new contracts and backlog expansion.

Supply agreements for gas-powered turbines, electrification equipment, and long-term service contracts play well into GEV’s model, which relies on long sales cycles and high-value equipment orders. Those trends are exactly the type that investors watch when valuing companies positioned for long-cycle infrastructure spending rather than short-term consumer demand.

Stock Performance and Valuation Considerations

The stock’s rally over the past year, roughly doubling from its post-IPO levels, shows that many investors have already priced in strong growth expectations. GEV’s share price hit all-time highs in late 2025 after dividend increases and capital return activity bolstered confidence, though some recent trading has been choppy as markets digest the latest earnings.

Even with robust results, some investors may hesitate due to GEV’s high current valuation and the fact that wind energy segments remain weak, with continued losses expected in offshore wind. Those segment challenges are part of the reason why some analysts urge a careful look at valuation multiples and long-term margin assumptions.

Is GEV a Buy Now?

Whether GEV is a buy at current levels depends on how investors view future demand and valuation:

Bullish case: Strong backlog, rising guidance, solid free cash flow, and structural demand for energy infrastructure (especially gas power and electrification) argue for continued growth. The raised 2026 and 2028 outlook suggests the company seesa long-term opportunity, which could support further stock appreciation if execution stays strong.

Caution points: A near-100% gain over the past year may already reflect a lot of positive expectations. Wind segment challenges, valuation multiples, and broader market risk appetite can temper near-term upside, so valuation discipline and watching execution against guidance will be key.

In simple terms: GEV’s earnings show the business is growing and well-positioned for continued infrastructure demand, but future returns depend on how well management turns backlog into profit and how markets value that growth at current stock prices.

Click Here for Updates on GEV – It’s 100% FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment. Please read our Full Disclaimer: https://dexwirenews.com/disclaimer/