General Mills (NYSE: $GIS), a global food company that markets and sells a wide array of food products, including snacks, cereals, and baking mixes, released its third quarter fiscal year 2025 results on Wednesday, March 19, 202,5, before markets opened. The giant food company reported a mixed bag of results; here is a breakdown of its Q3 results.

General Mills Q3 Results

For the third quarter of fiscal 2025, General Mills reported a 5% YoY decline in net sales to $4.8 billion, driven by lower pound volume and unfavorable FX, and below estimates of $4.96 billion. The company reported an adjusted EPS of $1, down 15% YoY but above estimates of $0.98. Net earnings were down 7% YoY to $626 million.

It reported a 60-basis point decline in the adjusted gross margin to 33.4%, primarily due to input cost inflation, unfavorable net price realization mix, and supply chain deleverage. General Mills reported a 2% decline in the operating profit to $891 million and an adjusted operating profit of $801, a 13% YoY decline for a 140-basis point decline in adjusted operating profit margin to 16.5%.

Segment Performance

Its North America Retail segment saw the biggest decline in net sales at 7%, while the North America Pet segment remained flat. Meanwhile, its North American Foodservice segment saw a 1% increase YoY, while the International segment saw a 4% YoY decline.

Other Q3 Highlights

General Reported $2.3 billion in cash from operating activities at the end of the nine months of fiscal 2025, compared to $2.4 billion the previous year. Capital investments came in at $405 million for the period, compared to $486 million the previous year.

It paid a dividend of $1 billion for the period, the same as last year, and bought back $902 million shares compared to $1.6 billion shares the previous year.

What The Leadership Had To Say

Commenting on the results, Jeff Harmening, Chairman and CEO of General Mills, stated, “Our third-quarter organic net sales finished below our expectations, driven largely by greater-than-expected retailer inventory headwinds and a slowdown in snacking categories. At the same time, we drove continued positive market share trends in Pet, Foodservice, and International as well as improvement in Pillsbury refrigerated dough and Totino’s hot snacks.”

The CEO added that the focus of General Mills was on improving sales growth through increased investment in brand communication, innovation, and consumer value. These initiatives would be funded by its ongoing cost saving measures.

Fiscal 2025 Outlook And Fiscal 2026 Cost Efficiency Forecast

General Mills announced a cut to its sales guidance for fiscal 2025. It now expects full-year net sales to fall 2% to 1.5% compared to the previous forecast of 0% to 1%. The adjusted operating profits and adjusted EPS are now expected to dip 8% to 7% from the previous range of a 4% to 2% decline.

The free cash flow conversion is, as the previous forecast, at least 95% of adjusted after-tax earnings. However, this forecast does include the potential impact of UAS tariffs.

The company is targeting at least a 5% saving in cost of goods sold for fiscal 2026 as part of its Holistic Margin Management program. This would represent around $600 million in savings. Additionally, it has begun a review of expected cost-saving initiatives with a target of at least $100 million in fiscal 2026.

General Mills (GIS) Market Performance

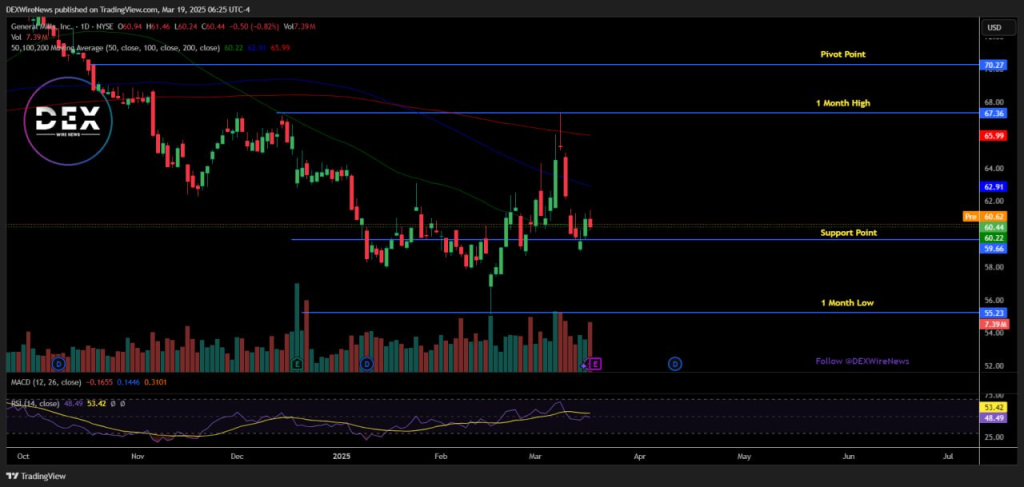

Following the revenue miss, and lowered guidance, GIS shares declined 3.98% in premarket trading to $58.09 on March 19, 2025 as of 8:41 AM EDT. Year to date, the stock is down 5.22% and down 10.78% in the past 12 months, as of Tuesday’s closing price.

As of Tuesday’s closing of $60.44, GIS is trading above its 50-day moving average of $60.22 but below its 200-day moving average of $65.99.

Analysts give GIS an overall hold rating. They forecast an average price of $65.00, which is 7a .54% upside based on Tuesday’s closing price. The analysts provide a wide range of forecasts, ranging from a high of $71 to a low of $58.

Should You Add GIS To Your Portfolio?

General Mills is one of the most diversified food companies in North America. While it missed revenue estimates, it beat EPS estimates, and its Holistic Margin Management cost-saving program could provide it with $600 million for expansion and marketing efforts.

However, its biggest headwinds could be Trump’s planned tariffs. Investors should keep a close eye on how it manages upcoming challenges. Based on its most recent results, and lowered full-year guidance, the analyst’s rating of hold could potentially be a great move in the medium term.

Click Here For Updates on GIS – It’s FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment.