Commercial Metals (NYSE: $CMC) is a leader in the recycling of scrap metal used in the manufacture and fabrication of steel products like wire rod, merchant bars, and rebars used in the construction sector. The company uses a vertically integrated model from scrap recycling to finished products. On Thursday, January 8, 2026, Commercial Metals released its Q1 results. Let us deep dive into those results.

Commercial Metals Q1 Results

For Q1, the company reported revenue of $2.12 billion, up 11% YoY, and beating estimates of $2 billion. It reported an EPS of $1.84, compared to $0.78 last year, and above estimates of $1.55.

The company reported a consolidated core EBITDA of $316.9 million, a 52% YoY increase, for a core EBITDA margin of 14.9%. It launched several new commercial and operational initiatives under its Transform, Advance, and Grow (“TAG”) program. This program has the goal of ending fiscal 2026 with an annualized run-rate EBITDA benefit of $150 million.

Strategic Investments

The company revealed that it had closed the acquisition of CP&P and Foley in December 2025, which will be an important growth platform in the precast concrete sector by deploying over $2.5 billion of capital. During the quarter, it also renamed the Emerging Business Group to Construction Solutions Group, which will include precast. That will better reflect the segment’s business composition.

The company expects these acquisitions to generate $240-$250 million in incremental annualized EBITDA. It expects synergies of $30-$40 million by the end of the third year. For fiscal 2026, it projects the precast business will contribute $165-$175 million to the adjusted EBITDA of Construction Solutions.

Segment Performance

Its North America Steel Group delivered strong results, with an adjusted EBITDA of $293.91 million, and a margin of 17.7%, up from 12.3% last year, representing the highest steel products margin over scrap in almost three years. The Europe Steel Group faced major challenges, generating $10.93 million, and a 4.4% margin, from 12.3 % last year.

The Construction Solutions Group reported net sales of $198.3 million, a 17.0% YoY increase, and adjusted EBITDA of $39.6 million, a 74.7% YoY increase, for an adjusted EBITDA margin of 20.0%.

Its positive results in North America were attributed to supportive policies, with domestic suppliers accounting for 89% of the US market. Current policies place a 50% tariff on all imports. That is in addition to anti-dumping duties, with further policy developments expected.

Balance Sheet And Capital Allocation

Following the acquisitions of precast businesses, CMC increased its net leverage to around 2.5x, but it has committed to lowering that below 2x in the next 18 months via disciplined capital allocation. It has outlined its approach to balancing growth investment, shareholder returns, and debt management.

The company bought back $38.9 million worth of shares in Q1, while continuing to invest in the TAG program, with $166.1 million remaining under its current share buyback program. It also declared a quarter dividend of $0.18.

The company ended Q1 with $3 billion in cash and cash equivalents, and nearly $1.9 billion in liquidity. Operating cash flow was $204.2 million, while long-term debt came in at $3.305 billion.

CMC Outlook

Company CEO Peter Matt said that they expect the core EBITDA to decline modestly in Q2 from Q1 levels. He added that the Europe Steel Group’s adjusted EBITDA is expected to be approximately breakeven, with margin growth potential in later quarters.

In Q2, the company will recognize several expenses related to acquisitions, including debt issuance costs, transaction fees, and customary purchase accounting adjustments, which will all be excluded from Core EBITDA.

The adjusted EBITDA for North America Steel Group is expected to decline sequentially, driven by seasonality and maintenance, while steel product margins are expected to remain relatively stable. It expects results for Construction Solutions Group to improve, driven by contributions from precast.

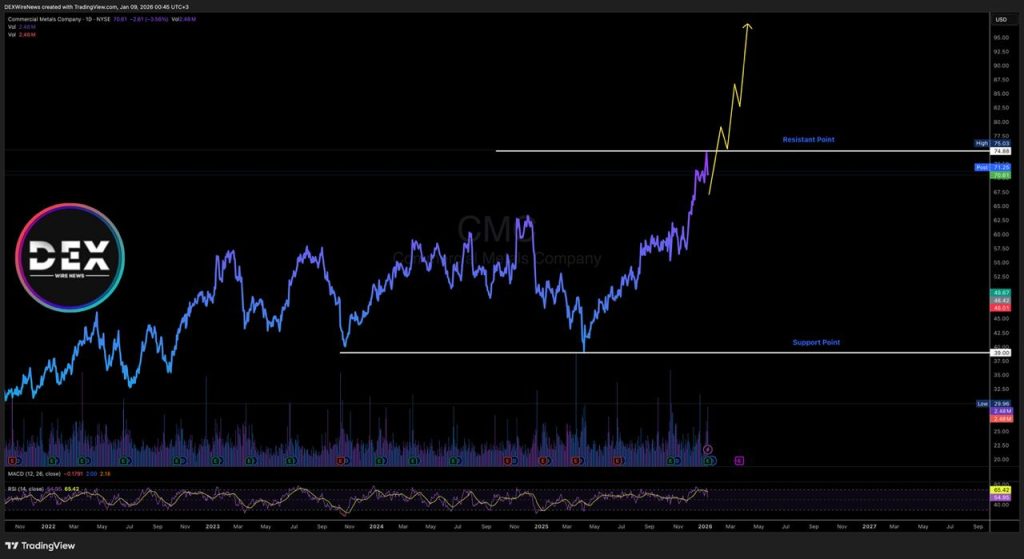

Commercial Metals (CMC) Market Performance

Following the expected non-profit hits from acquisitions and seasonal decline, CMC’s shares declined 2.29% during the Thursday trading session to $71.54 as of 3:09 PM in New York. The stock is trading near its 52-week high of $75.03.

Year to date, CMC shares are up 3.28%, while over the past six months, the shares are up 37.59%. Over the past 12 months, the stock price has appreciated 50.28%. The current stock price is above both the 50- and 200-day moving averages of $64.73 and $54.97, respectively.

Analysts remain optimistic about the future of $CMC, issuing a moderate buy rating for the stock. They forecast an average price of $79.11, which is a 12.40% upside. The analysts give a wide range of forecasts, with a high of $85 and a low of $71.

Is Now The Time To Add CMC To Your Portfolio?

Given the analysts’ positive sentiment and the expected synergies from the precast acquisitions, adding CMC to your portfolio could potentially lead to some great long-term gains.

Click Here for Updates on CMC – It’s 100% FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment. Please read our Full Disclaimer: https://dexwirenews.com/disclaimer/