Snowflake (NYSE: $SNOW) is a data cloud company offering a platform that functions as the technological backbone for the data cloud. The platform empowers users to centralize data into a single, reliable source to derive meaningful business insights, construct data applications, and facilitate the sharing of data and data products. It also supports data warehousing, data lakes, Unistore, collaboration, data engineering, cybersecurity, data science, and machine learning.

On Wednesday, May 22nd, Snowflake reported impressive first-quarter fiscal 2025 results that ended April 30, 2024. The short interest in SNOW has ticked up marginally to 9.74 million shares as of April 30, 2024, representing 3,01% of the float, and 2.91% of the shares outstanding.

Key Financial Highlights

Revenue for the quarter reached $828.7 million, representing a remarkable 34% year-over-year growth and a 5.4% beat. The company’s core product revenue surged to $789.6 million, a 34% increase compared to the same period last year. it reported an EPS of $0.14, missing estimates of $0.17.

Furthermore, Snowflake reported a strong non-GAAP product gross profit of $607.3 million, boasting a healthy 77% margin. Non-GAAP operating income reached $36.2 million, or 4% of revenue, while adjusted free cash flow stood at an impressive $365.7 million, translating to a robust 44% margin.

Sridhar Ramaswamy, CEO of Snowflake, expressed his satisfaction with the company’s performance: “We finished our first quarter with strong performance across many of our key metrics. Product revenue was up 34% year-over-year at nearly $790 million, while remaining performance obligations were $5.0 billion, up 46% year-over-year. Our core business is very strong.”

Customer Growth and Retention

Snowflake’s customer base continues to expand, reflecting the growing demand for its AI Data Cloud solutions. Notably, the company now boasts 485 customers with trailing 12-month product revenue greater than $1 million, a 24-customer increase from the previous quarter. Also, Snowflake’s net revenue retention rate stood at an impressive 128%, indicating strong customer satisfaction and loyalty.

The company’s Forbes Global 2000 customer count also saw an 8% year-over-year increase, reaching 709 customers, further firming its position among the world’s largest enterprises.

AI and Strategic Acquisitions

Ramaswamy emphasized the company’s focus on artificial intelligence (AI), stating, “Our AI products, now generally available, are generating strong customer interest. They will help our customers deliver effective and efficient AI-powered experiences faster than ever.”

In line with its AI ambitions, Snowflake announced its intent to acquire certain technology assets and hire key employees from TruEra, an AI observability platform. This acquisition will enhance Snowflake’s capabilities in evaluating and monitoring large language model (LLM) applications and machine learning models in production.

Snowflake’s Upbeat Guidance

Snowflake’s strong Q1 performance has translated into an optimistic outlook for the remainder of the fiscal year. For the second quarter, the company expects product revenue in the range of $805 million to $810 million, representing a robust 26% to 27% year-over-year growth.

Snowflake has raised its product revenue guidance for the full fiscal year to $3.3 billion, reflecting a 24% increase over the previous fiscal year. The company also expects a non-GAAP product gross profit margin of 75%, a non-GAAP operating margin of 3%, and an adjusted free cash flow margin of 26%.

Industry Tailwinds and Competitive Landscape

Snowflake’s success is underpinned by the growing demand for cloud-based data warehousing and analytics solutions, driven by the increasing volume and complexity of data generated by businesses across various industries. As companies seek to leverage data for informed decision-making and gain a competitive edge, solutions like Snowflake’s AI Data Cloud become increasingly valuable.

However, the company faces stiff competition from established and emerging players in the data analytics and cloud computing space. Major tech giants, such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform, offer their own data warehousing and analytics solutions, posing a significant challenge to Snowflake’s market dominance.

Also, the rise of generative AI and large language models has attracted significant investment and competition from companies like OpenAI, Google, and Microsoft, potentially impacting Snowflake’s AI aspirations.

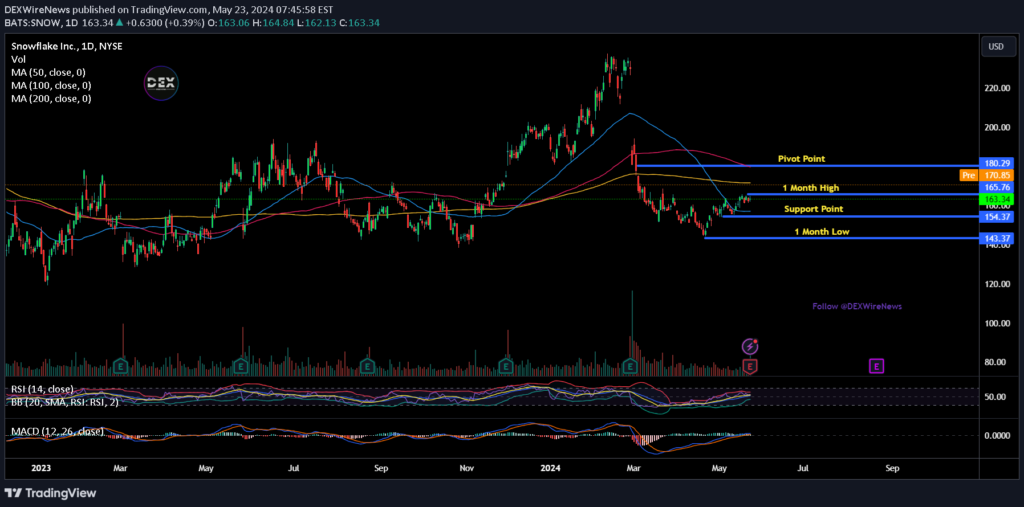

Snowflake (SNOW) Stock Performance

Following Snowflake’s (SNOW) results earnings miss, the stock experienced a 2.80% to $158.77 as of 12:09 PM EDT. The day’s range has fluctuated between $155.40 and $168.80, as the market weighs Snowflake’s ability to sustain its momentum and execute its AI strategy effectively. YTD the stock is down 16.09%, and over the past 52 weeks, it has sunk 9.40%.

Should You Buy Snowflake (SNOW) Stock in 2024?

Snowflake’s impressive first-quarter performance, with a 34% year-over-year revenue growth and strong customer retention, highlights its strong business fundamentals. Also, the company’s strategic focus on AI, including the acquisition of TruEra’s assets, positions it well to capitalize on the burgeoning AI market.

However, the competitive landscape remains intense, with tech giants like AWS, Microsoft, and Google offering competing solutions. Before making this decision, carefully evaluate Snowflake’s ability to maintain its growth trajectory, execute its AI strategy effectively, and differentiate itself in the crowded data analytics market.

Click Here for Updates on Snowflake – It’s FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment.