Micron Technology (NASDAQ: $MU), one of the most notable names in the tech sector, released its Q4 fiscal 2024 results on Wednesday after markets closed. The stock soared in pre-market trading after beating estimates. Here is a deep dive into the results.

Micron Technology Beats Estimates In FQ4 Results

The computer memory and data storage giant reported revenue of $7.8 billion in the fourth quarter, a 14% increase from Q3 and a 93% increase YoY, beating estimates of $7.6 billion. Earnings for the quarter came in at $1.18 on a non-GAAP net income of $1.34 billion, beating estimates of $1.13 per share.

Other Financial Highlights

Micron Technology reported an operating cash flow of 3.41 billion compared to $2.48 billion in Q3 and $249 million in the same period last year. It ended the quarter with a free cash flow of $323 million and $9.2 billion in cash and investments.

The company ended the quarter with a non-GAAP gross margin of 36.5%, an over 8 percentage point increase from Q3, and an over 27 percentage point increase from the same period last year. Its non-GAAP operating margin came in at 22.5% compared to 13.8% in the third quarter and an operating margin loss of 30.1% the previous year.

Fiscal 2024 Performance

In fiscal 2024, Micron Technology’s revenue came in at $25.1 billion, a 62% YoY increase while the non-GAAP EPS came in at $1.30 per share. It ended the year with $386 in free cash flow, and operating cash flow of $8.5 billion.

Segment Performance

Micron Technology’s DRAM segment brought in revenue of $5.3 billion in Q4, a 93% YoY increase, while the NAND segment brough it $2.4 billion in revenue, a 96% YoY increase.

Commenting on the results, Micron Technology CEO Sanjay Mehrotra said, “Micron delivered 93% year-over-year revenue growth in fiscal Q4, as robust AI demand drove a strong ramp of our data center DRAM products and our industry-leading high bandwidth memory. Our NAND revenue record was led by data center SSD sales, which exceeded $1 billion in quarterly revenue for the first time.”

Share Buyback And Dividend

At the end of Q4, Micron Technology had bought back $300 worth of shares for FY24. Since FY21, the company has bought back $4.4 billion worth of shares.

It announced a dividend of $0.115 per share, to be paid out on October 23. Micron Technology has paid out $1.5 billion in dividend to shareholders since FY21. In total, it has returned $5.9 billion to shareholders via share repurchases, and dividends.

Micron Technology Issues Guidance

For the first quarter of fiscal 2025, Micron Technology expects revenue of $8.5 to $8.9 billion, well above analysts’ estimate of $8.32 billion in revenue. It expects a non-GAAP EPS of $1.74 at the midpoint, well above estimates of $1.52. Additionally, it expects a gross margin 39.5% at the midpoint, above analysts’ forecast of 37.7%. It expects operating expenses of $1.085 billion at the midpoint.

The company expects that high bandwidth memory (HBM) chips, widely used in the AI industry, will drive growth in Q1 fiscal 2025. During the earnings call, Micron Technology CEO Sanjay Mehrotra stated, “We delivered several hundred million dollars of revenue in fiscal year ’24, and we look forward to delivering multiple billions of dollars of revenue of HBM in fiscal year ’25.”

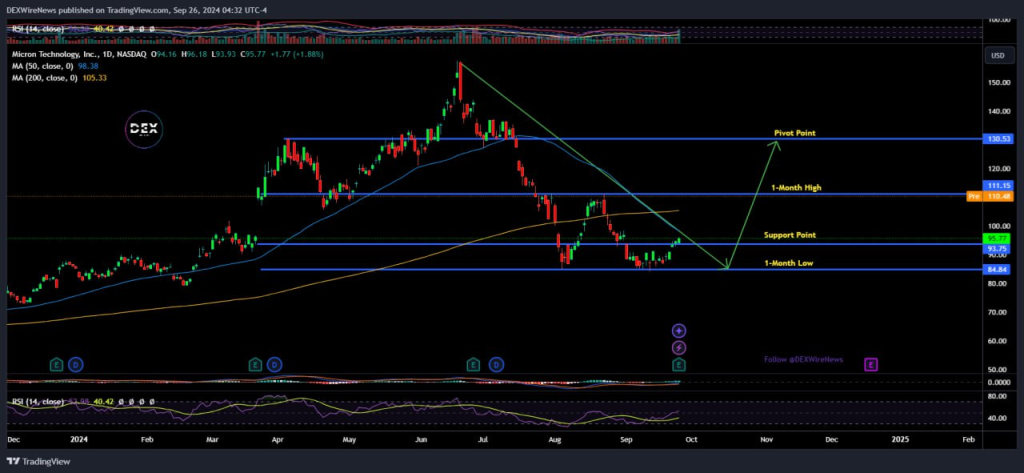

Micron Technology (MU) Market Performance

Following the stellar Q4 results, MU shares soared 16.74% in pre-market trading to $111.80 per share. Based on the Wednesday closing price of $95.77, MU shares are up 12.22% year to date and up 39.65% in the past 12 months. The stock has underperformed the market in the last month, sinking 6.9%, compared to the 1.7% gain of the S&P 500 in the same period.

Analysts are optimistic about MU, giving it a strong buy rating. They forecast a wide range of price targets, ranging from a high of $225 to a low of $67. Their average price target of $151.54 is a 58.23% upside from the last closing price of $95.77 per share.

Should You Add MU To Your Portfolio?

Micron Technology, like other stocks in the semiconductor sector, is highly cyclical. Despite these dips and rises, MU’s overall trajectory is upward. Malmanagement predicts fiscal 2025 will be a year of growth driven by a robust AI industry.

Consequently, while MU shares have seen massive gains in recent years, there is still a massive upside potential. Investing in the stock as part of a long-term strategy could potentially pay off.

Click Here For Updates on Micron Technology – It’s FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment.