Zoom Video Communications, Inc. (NASDAQ: $ZM) is a communications tech company based in San Jose, CA that operates Zoom, the unified communications platform. Zoom allows users to connect via video, audio, chat, and phone across multiple devices. Its features include Whiteboard, Workspace, Team Chat, Meetings, Phone, and AI solutions.

On Monday, May 20, 2024, Zoom Video Communications released its Q1 results for fiscal 2025 to a negative market reaction.

Zoom Beats Revenue and Earnings Estimates in Q125 Results

Zoom reported revenue of $1.14 billion in the first quarter, beating estimates of $1.13 billion, representing 3.2% Y/Y growth. It reported an adjusted EPS of $1.35, beating estimates of $1.20, representing the seventh quarter in a row Zoom has beaten EPS estimates.

Operating cash flow in the first quarter was up 40.6% Y/Y to $588.2 million, while free cash flow was up 43.6% to $569.7 million. As of the end of the quarter, it had $7.4 billion in total cash.

Key Financial Highlights

The company saw enterprise revenue increase 5.3% Y/Y to $665.7 million. It reported a GAAP operating margin of 17.8% compared to 0.9% in Q124 while the non-GAAP operating margin came in at 40% compared to 38.2% the previous year.

The company ended the quarter with around 191,000 enterprise customers, below estimates of 223,328. Of those, 3,883 brought in over $100K in TTM revenue, below estimates of 3,957.

The company reported $3.67 billion in Remaining Performance Obligations (RPO), compared to estimates of $3.64 billion.

By region, the Asia-Pacific region saw a 2.1% decline in revenue to $138 million, below estimates of $140.20 million. The EMEA region saw a 2.2% increase in revenue to $184 million, beating estimates of $171.59 million. In the Americas, Zoom saw a 4.3% increase in revenue to $819 million, beating estimates of $813.89 million.

Leadership Team Comments

Commenting on the results, Eric Yuan highlighted the success their AI product, Zoom Workplace, had enjoyed thus far. He stated, “We are so pleased to see more customers adopting our Zoom Workplace and Business Services products in order to reap the benefits of our modern, natively integrated, AI-powered technologies.”

Zoom CFO Kelly Steckelberg said AI would continue to be a priority for the company. She said, “Embedding AI across all aspects of Zoom Workplace and Business Services is a key priority as we continue to drive productivity and engagement for our customers.”

Zoom Q2 and Fiscal 2025 Guidance

For the second quarter of fiscal 2025, Zoom forecasts revenue of $1.145 billion to $1.15 billion, missing estimates of $1.15 billion at the midpoint.

The company forecasts a non-GAAP income from operations of $415 million to $420 million and a non-GAAP diluted EPS of $1.20 to $1.21.

For the full year, Zoom expects revenue of $4.461 billion to $4.62 billion. The non-GAAP income from operations is forecast to be $1.74 billion to $1.75 billion for a non-GAAP diluted EPS of $4.99 to $5.02.

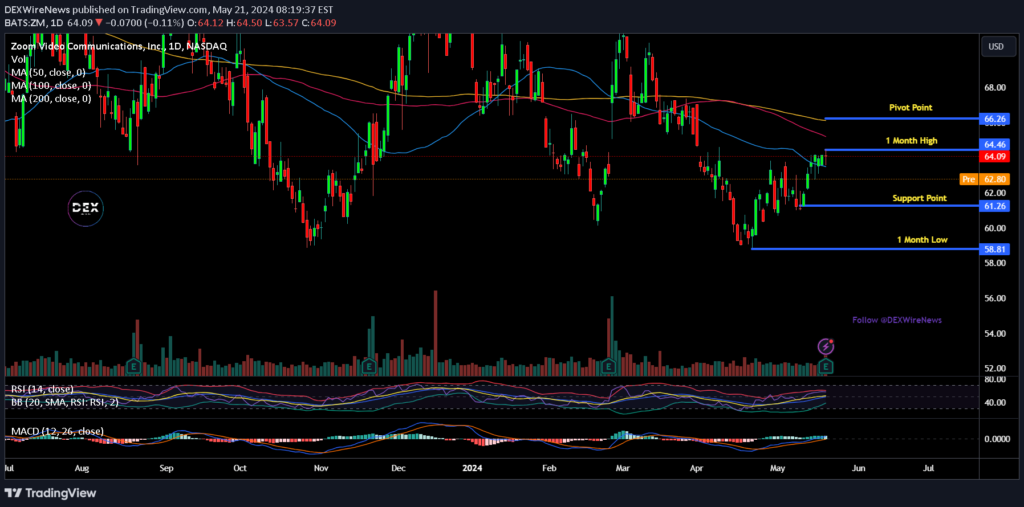

Zoom (ZM) Stock Performance

Following the guidance miss, ZM shares sank 1.82% a few minutes after the opening bell to $62.92 as of 09:47 AM EDT.

Over the past month, Zoom stock is up 7.64%, beating the SPX, which is up 5.94% in the same period. However, Zoom is down 7.32% compared to the 14.07% gain of the Technology sector in the same period. Zoom is down 10.25% in the past 523 weeks compared to the 26.61% gain of the SPX in the same period.

Short sellers hold around 12.76 million ZM shares as of April 30, 2024, representing 4.83% of the floating shares and 4.11% of the shares outstanding. The shares are trading below the 50 DMA and 2300 DMA of $63.50 and $66.12, respectively.

Analysts’ Outlook on ZM Stock

According to 24 stock analysts, Zoom has an overall hold rating. The analysts forecast a wide range for the stock, with a high of $95 and a low of 62. Their average price target of $77.89 is a 23.63% upside from the most recent price.

Is Zoom A Buy?

During the pandemic, Zoom was among the hyper-growth stocks. It became a favorite of people around the world as a means to work remotely amid restrictions.

In fiscal 2021, it saw revenue soar 326%, while in fiscal 2022, revenue soared 55%. The company saw revenue rise 7% in fiscal 2023, as the pandemic measures were lifted. As post-pandemic headwinds forced companies to cut down on spending, Zoom saw revenue slow down, and in fiscal 2024, revenue rose 3.1%.

The slowdown in revenue since the pandemic has led investors to conclude that the era of hypergrowth is over, and the stock has declined sharply from its high of over $568 in October 2020. For fiscal 2025, the company expects revenue to grow 2%.

However, the company is integrating AI features, which could improve efficiency of large enterprises that accounted for 58% of its revenue in 2024. However, analysts do not expect those features to lead to the hyper growth of its top line witnessed during the pandemic.

While Zoom’s business has stabilized, it will need to make huge acquisition to grow its revenue base or attract a takeover from a major buyer to become attractive to investors. Until then, the hold rating by analysts accurately represents the stock’s potential performance in the medium term.

Click Here for Updates on Zoom – It’s FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment.