Airbnb (NASDAQ: $ABNB) stock fell over 14% on Wednesday morning following the release of its second quarter results. The revolutionary tech company, which has revolutionized the travel industry, failed to meet investor’s expectations.

Airbnb Posts Mixed Second Quarter Results

In its second quarter fiscal 2024 results, Airbnb posted revenue of $3.75 billion, an 11% year over year increase, beating estimates of $2.74 billion. Meanwhile, net income fell 14.62% year over year to $555 million for an EPS of $0.86. The EPS missed estimates of $0.95 by 10%, triggering selloff of the stock.

Margins also fell with the net income margin dropping to 20% from 26% the previous year. The company’s trailing twelve-month free cash flow came in at $4.3 billion for a free cash flow margin of 41%, compared to 43% the previous year.

During the quarter, the company bought back $749 million worth of shares. It announced that it had $5.25 billion remaining under its current share buyback scheme.

Other Performance Metrics

The company reported a 25% year over year in app download, with the US leading the growth. It also reported continued growth of first-time bookers, with most growth coming from the young demographics.

The company reported $1.1 billion in net cash from operations for the quarter, and $1 billion in free cash flow. It ended the quarter with $11.3 billion in liquidity. Additionally, they had $10.3 worth of funds held on behalf of guest at the end of the quarter.

Outlook Misses Estimates

For the third quarter, Airbnb expects sales of $3.67 billion to $3.73 billion, below estimate of $3.84 billion. The company stated that it expected shorter booking windows, signaling travelers were waiting until the last minute due to economic worries.

It also said it expected the adjusted EBITDA margin to fall compared to last year, while marketing costs are expected to grow faster than revenue year over year. For the full year, the expect an adjusted EBITDA margin of 35%.

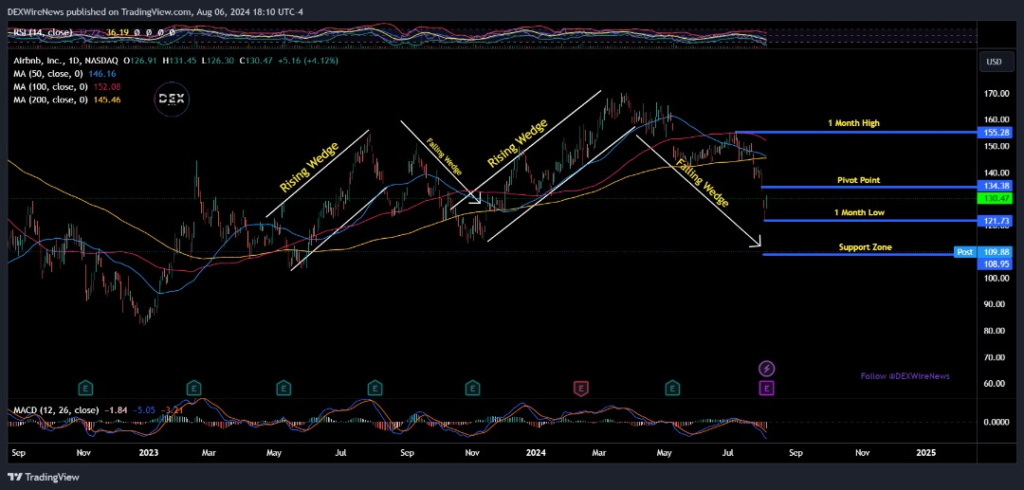

Airbnb Stock Plummets Amid Recession Fears

Investors have been closely watching the market for signs of falling consumer demand as the Fed held off on cutting rates in July. Thus far, the signs are not promising.

For example in its Q2 results, McDonald’s (MCD) reported a 1% decline in comparable sales years over year compared to 11.7% growth the previous year. The company warned that consumers were “more discriminating” due to the state of the economy.

ABNB has had a bad run in 2024, falling 2.98% as of Tuesday’s closing, compared to the S&P 500, which has gained 10.48%. Industry peers Booking Holdings (BKNG) and Expedia (EXPE) have also underperformed falling 1.28% and 20.99% in the same period.

The travel industry has faced challenges as macroeconomic challenges have forced consumers to cut back. Additionally, the growing impact of geopolitical conflict have hurt the sector.

ABNB has an elevated valuation compared to industry peer. Its forward P/E ration of 29.5 is much higher than that of Bookings Holdings (BKNG) and Expedia (EXPE) of 19.61 and 10.05 respectively.

Should You Buy Or Hold ABNB Stock?

Airbnb’s results this quarter fell below estimates, driven by wider macroeconomic issues. However, the company is still expanding its global foot print, and continues to enter new markets.

The company is likely to continue experience volatility in the short term amid macroeconomic challenges. There is also increased competition in the online bookings marketplace, which could challenge its dominant position.

Based on these reasons, those who already have a position in the stock should consider holding int it. However, new investors should potentially watch on the sidelines for macroeconomic factors to improve.

Click Here For Updates on Airbnb – It’s FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment.