Okta, Inc. (NASDAQ:$OKTA) operates an identity management platform that enables enterprises to connect their employees and customers to technology resources securely. Based in San Francisco, Okta’s cloud-based single sign-on and multi-factor authentication solutions allow users to access web and mobile applications securely from various devices.

Okta recently reported solid fourth-quarter and fiscal 2024 results for the year ended January 31, 2024, driven by a high demand for identity access management solutions. The company generated revenue that surpassed Wall Street estimates.

Q4 Financial Results Beat Estimates

Okta reported better-than-expected financial results for the fourth quarter and fiscal year 2024. Revenue grew 19% year-over-year to $605 million, surpassing analysts’ estimates of $587.6 million. Subscription revenue, which accounts for most of the revenue, rose 20% to $591 million.

The company posted non-GAAP net income of $113 million, or $0.63 per diluted share, significantly higher than $52 million, or $0.30 per share, in the year-ago quarter and above expectations of $0.51 per share. Okta generated a record free cash flow of $166 million in Q4, representing 28% of revenue and a surge of 129% year on year.

For the full 2024 fiscal year, Okta grew revenue by 22% to $2.263 billion. The company swung to a non-GAAP profit of $286 million from a slight loss last year, while free cash flow surged to $489 million from $65 Million.

Okta Forecasts Slowed Growth

While Okta beat Q4 estimates, its guidance indicates slowing growth ahead. For Q1 fiscal 2025, the company expects 16% to 17% revenue growth of $603 million to $605 million. For the full 2025 fiscal year, the company forecasts revenue of $2.495 billion to $2.505 billion, representing growth of 10% to 11%. This projected slow growth reflects Okta’s large size and uncertain economic environment, according to CFO Mike Kourey.

Improved Profitability

Despite the slower top-line expansion, Okta aims to drive significant margin improvements in fiscal 2025. It guided for an 18% to 19% non-GAAP operating margin for the year, margin expansion. This demonstrates its ability to leverage its operating scale even with moderating revenue growth.

The company does face some near-term headwinds from its October 2023 security incident and related investigation costs. However, the financial impact appears manageable, and Okta remains well-positioned to gain identity management market share in the long term.

Market Reaction

While multiples have contracted significantly, Okta’s guidance shows it remains a premium growth story. Investors are willing to pay for identity management exposure, but further deceleration could warrant additional multiple compression.

The quarter supports Okta’s best-in-class identity platform and ability to drive margin expansion over time. But a worsening macro backdrop makes it prudent to temper top-line expectations. Okta offers a quality secular growth pick, albeit likely at a premium valuation relative to software peers.

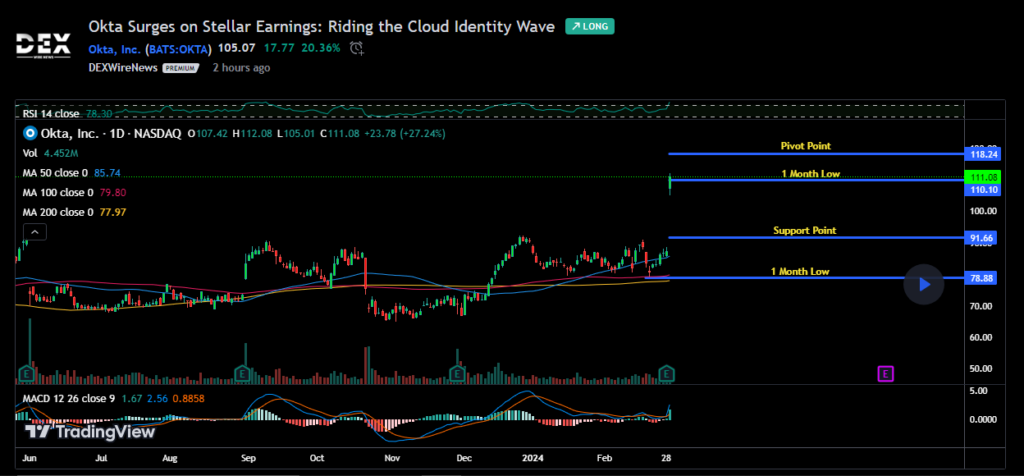

Okta Stock Performance

Okta shares closed at $87.30 on February 29th, 2024, up $0.39 or 0.45% during the trading session. The modest gain continues the stock’s recent upward momentum after a significant sell-off in 2022. Over the past two years, Okta stock has plunged over 70% from all-time highs as part of the broader decline in technology valuations. However, the identity management leader has rebounded nearly 20% off November 2023 lows.

Investor optimism stems from the fourth-quarter beat and improved profitability outlook, which have supported the recent recovery. Nonetheless, the stock still carries a multiple premium, with a forward P/E ratio of 44.05. While macro uncertainty persists, Okta offers long-term growth potential in digital identity. But further deceleration could warrant additional compression of its elevated valuation multiples.

Is Okta Stock a Buy in 2024?

Despite high volatility, Okta remains well-positioned to capitalize on the long-term digital identity trend. While revenue growth is decelerating, the company projects solid margin expansion as it leverages operating scale. Okta also reported impressive free cash flow, giving it flexibility to drive growth and return capital.

However, valuation remains a crucial concern, with shares trading over ten times the revenue amid macro uncertainty. Further, top-line slowdown or market deterioration could warrant additional compression. For investors comfortable with high multiples, Okta offers quality secular growth exposure.

However, more risk-averse investors may prefer to see improved profitability and stabilization in growth rates before building a position. Ultimate Okta’s premium multiple leaves the stock’s buy case dependent on one’s investment time horizon.

Click Here for Updates on Okta – It’s 100% FREE to Sign Up for Text Message Notifications!

Disclaimer: This website provides information about cryptocurrency and stock market investments. This website does not provide investment advice and should not be used as a replacement for investment advice from a qualified professional. This website is for educational and informational purposes only. The owner of this website is not a registered investment advisor and does not offer investment advice. You, the reader / viewer, bear responsibility for your own investment decisions and should seek the advice of a qualified securities professional before making any investment.